|

Business Paper Late Reports Ordinary Council Meeting

Council Chambers, Gundagai

6:00 PM, Tuesday 24th November, 2020

Administration Centres: 1300 459 689 |

|

Business Paper Late Reports Ordinary Council Meeting

Council Chambers, Gundagai

6:00 PM, Tuesday 24th November, 2020

Administration Centres: 1300 459 689 |

|

Ordinary Council Meeting Agenda |

24 November 2020 |

|

Ordinary Council Meeting Agenda |

24 November 2020 |

LATE REPORTS

1.1 I2S Inland Rail Community Consultative Committee

1.1 Monthly Finance Report for October 2020

1.2 September 2020 Quarterly Budget Review Statement

1.1 Referral of Financial Statements for Audit

|

Ordinary Council Meeting Agenda |

24 November 2020 |

|

DOCUMENT NUMBER |

339823 |

|||

|

REPORTING OFFICER |

Phillip McMurray, General Manager |

|||

|

AUTHORISING OFFICER |

Phillip McMurray, General Manager |

|||

|

RELEVANCE TO COMMUNITY STRATEGIC PLAN |

|

|||

|

FINANCIAL IMPLICATIONS |

There are no Financial implications associated with this report. |

|||

|

LEGISLATIVE IMPLICATIONS |

There are no Legislative implications associated with this report. |

|||

|

POLICY IMPLICATIONS |

There are no Policy implications associated with this report. |

|||

|

Nil |

|

Council endorse Councillor Bowden as Council’s Councillor representative on the I2S Inland Rail Community Consultative Committee. |

Discussion

Local government representation is best served by having two representatives, one councillor and a relevant staff person. However, the decision ultimately resides with Council to nominate who their representatives should be.

Council’s current representatives are Sharon Langham and Mark Ellis. Cr. Leigh Bowden, had expressed an interest in being a representative and attending our meetings which occur quarterly.

|

24 November 2020 |

|

DOCUMENT NUMBER |

339806 |

|||

|

REPORTING OFFICER |

Tim Swan, Manager Finance and Customer Service |

|||

|

AUTHORISING OFFICER |

Phillip McMurray, General Manager |

|||

|

RELEVANCE TO COMMUNITY STRATEGIC PLAN |

|

|||

|

FINANCIAL IMPLICATIONS |

Regular monitoring of Council’s finances will ensure that any issues are identified in a timely manner. |

|||

|

LEGISLATIVE IMPLICATIONS |

There are no legislative implications associated with this report. |

|||

|

POLICY IMPLICATIONS |

There are no policy implications associated with this report. |

|||

|

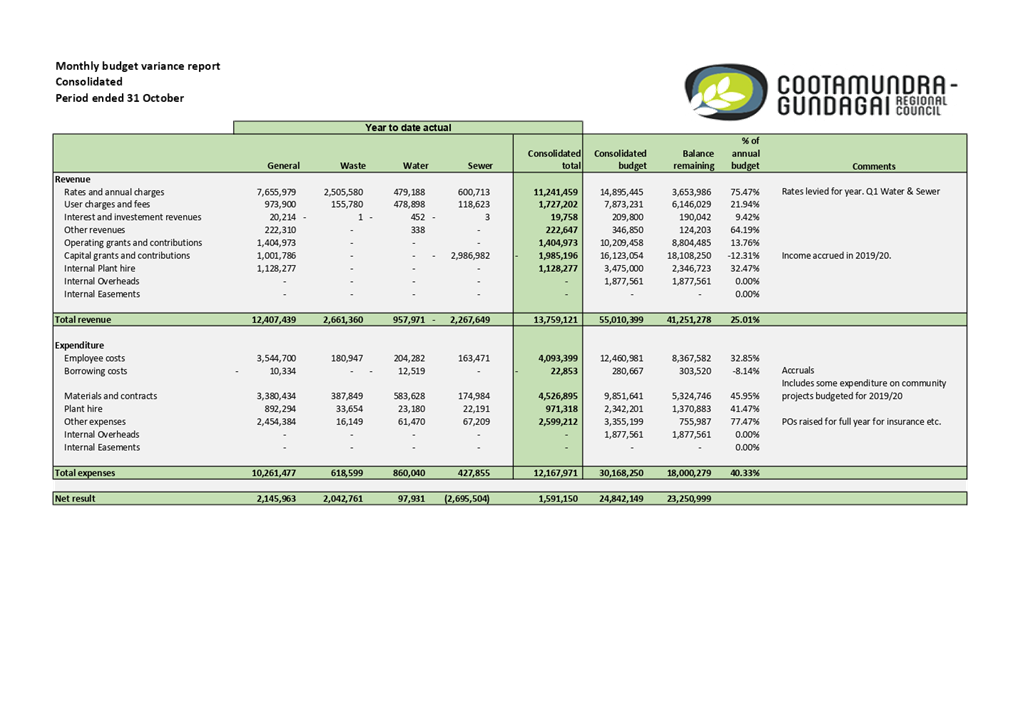

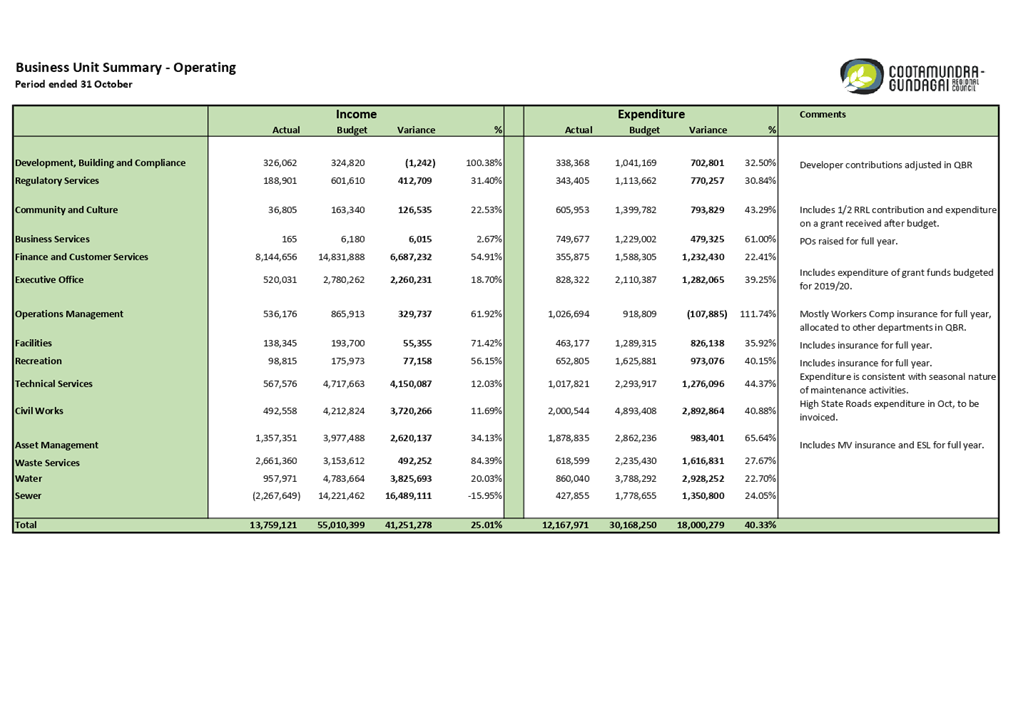

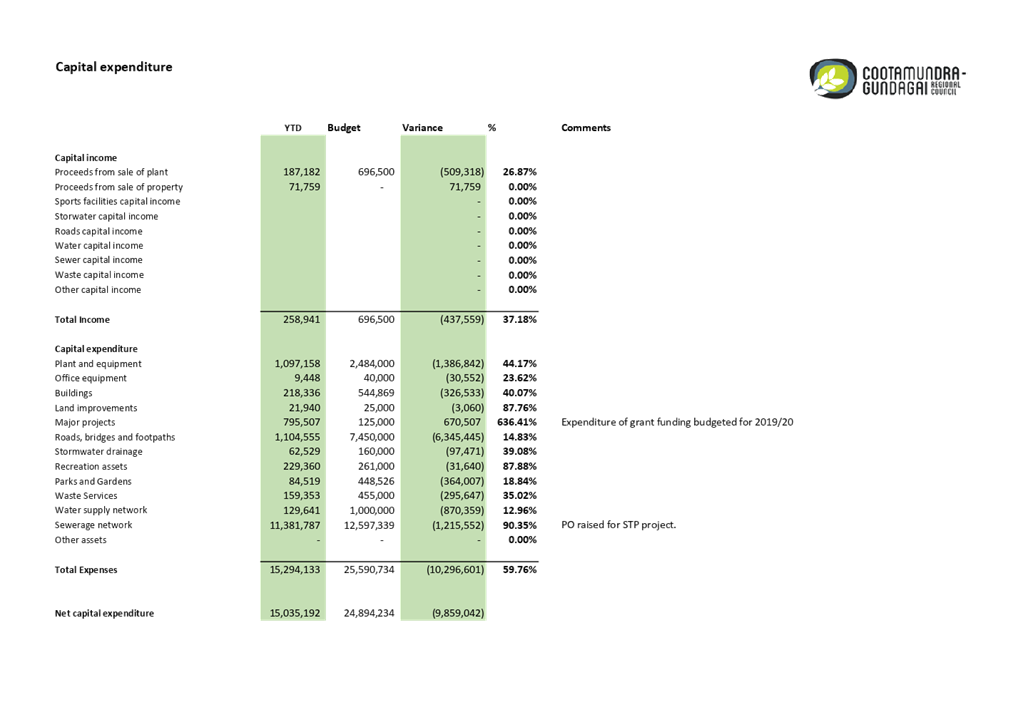

1. October 2020 Finance Report ⇩ |

|

That the Finance Report for October 2020 be received and noted. |

Introduction

The Monthly Finance Report provides Councillors with an update on the current budget status.

Discussion

No budgetary concerns have been identified. Expenditure is at 40% of budget, but this relates to payments and commitments for annual expenses.

Several anomalies will be resolved by the adoption of the September Quarterly Budget Review, and the rolling forward of unexpended grants from 2019/20.

|

24 November 2020 |

|

DOCUMENT NUMBER |

339820 |

|||

|

REPORTING OFFICER |

Tim Swan, Manager Finance and Customer Service |

|||

|

AUTHORISING OFFICER |

Phillip McMurray, General Manager |

|||

|

RELEVANCE TO COMMUNITY STRATEGIC PLAN |

|

|||

|

FINANCIAL IMPLICATIONS |

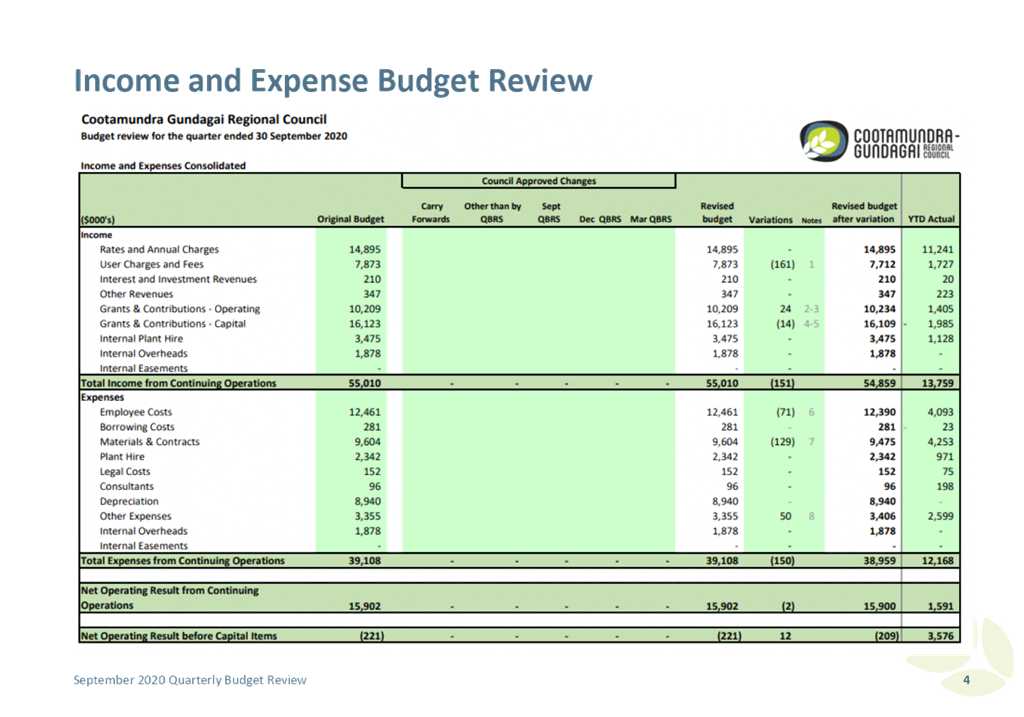

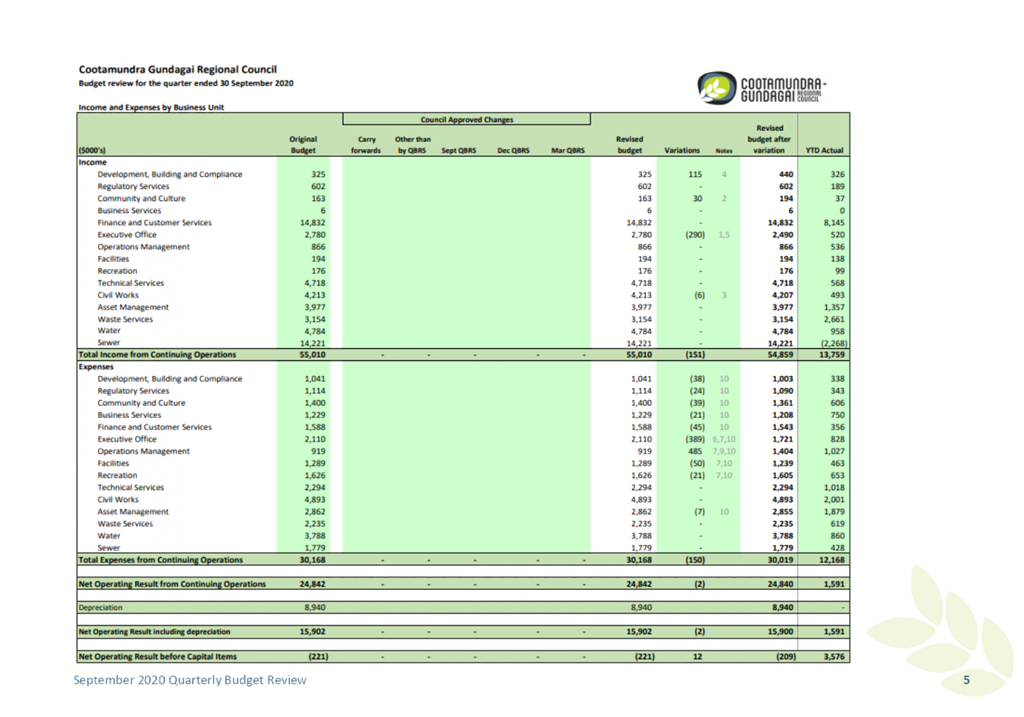

As reported in the attached quarterly budget review, the revised net operating result for the year to 30 June 2021 is a profit of $15,590,000. The budget adjustments recommended to Council for approval in this report result in a net change to the operating result of -$2,000. |

|||

|

LEGISLATIVE IMPLICATIONS |

Clause 203(1) of the Local Government (General) Regulation requires that, not later than 2 months after the end of each quarter, excluding the June quarter, the responsible accounting officer must submit a budget review statement to Council. The format of the review must be consistent with the minimum requirements contained in the Quarterly Budget Review Statement Guidelines provided by the Office of Local Government. |

|||

|

POLICY IMPLICATIONS |

There are no Policy implications associated with this report. |

|||

|

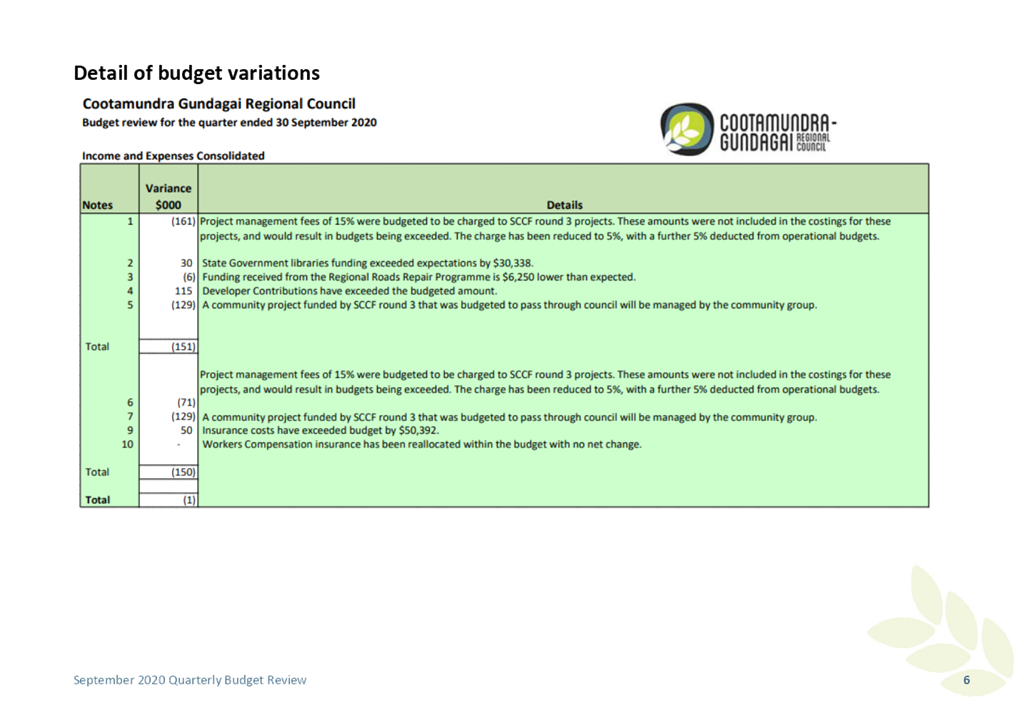

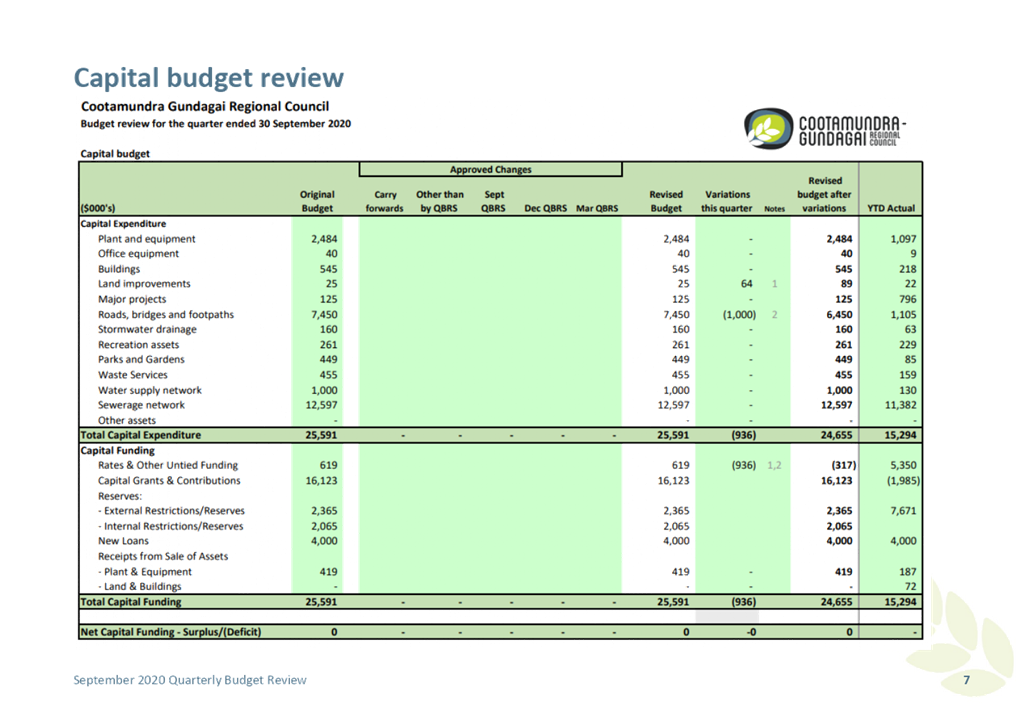

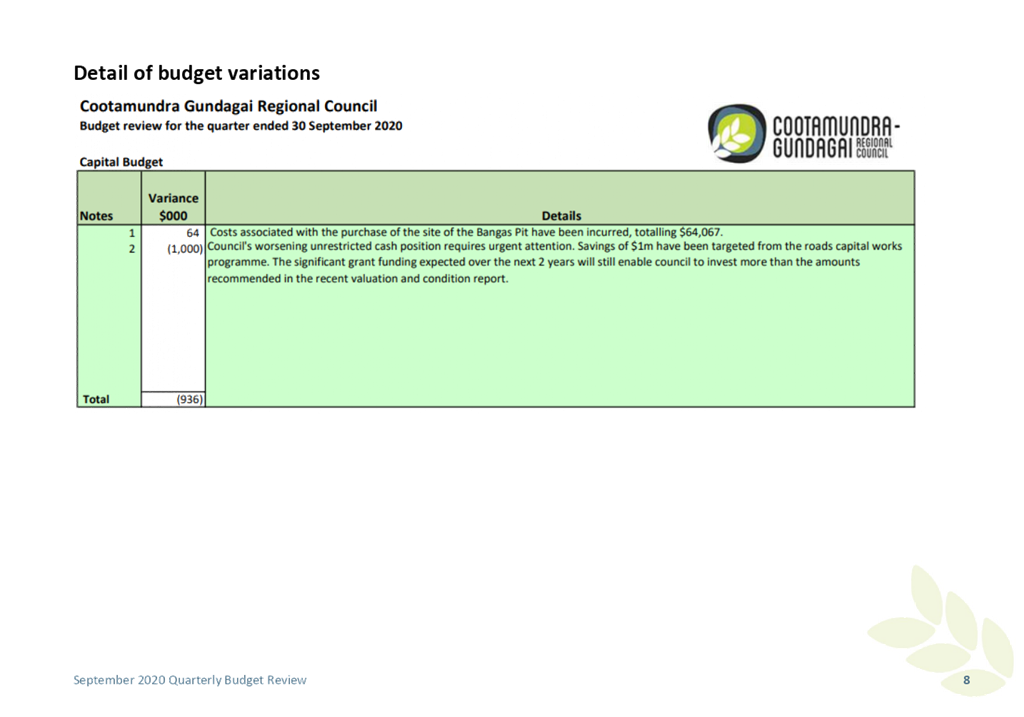

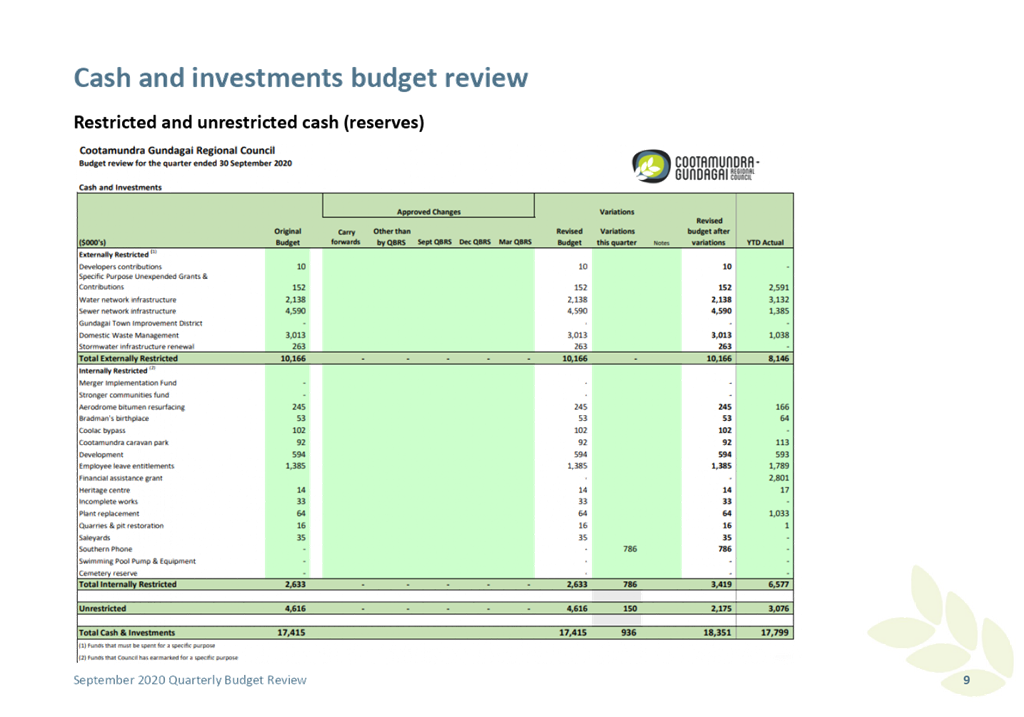

1. Quarterly Budget Review Report - September 2020 ⇩ |

|

1. That the September 2020 Quarterly Budget Review Report be received. 2. The budget variations listed in the report be adopted. |

Introduction

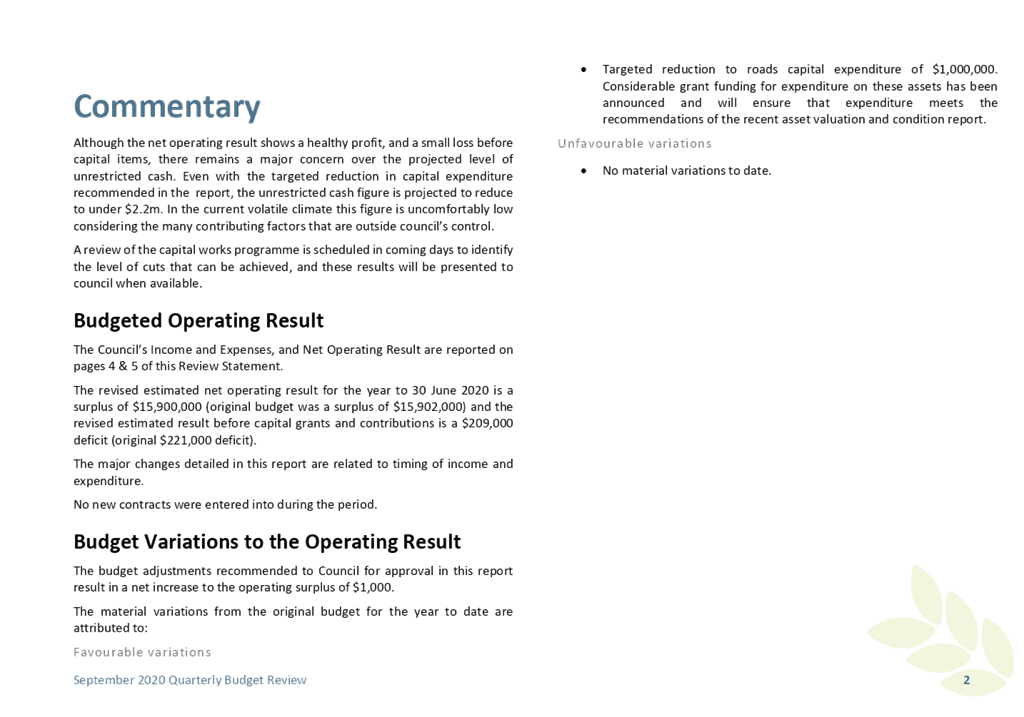

The purpose of this report is to present a summary of Council’s financial position at the end of the quarter, and to report on progress made against the original budget adopted by Council in its 2020-21 Operational Plan. A detailed list of budget variances is included in the attached Quarterly Budget Review, and these are presented for adoption by Council.

Discussion

Detailed commentary on the individual variations is included in the report itself. The net change to the projected operating result is a decrease of $2,000 to a surplus of $15,900,000.

|

24 November 2020 |

|

DOCUMENT NUMBER |

339840 |

|||

|

REPORTING OFFICER |

Tim Swan, Manager Finance |

|||

|

AUTHORISING OFFICER |

Phillip McMurray, General Manager |

|||

|

RELEVANCE TO COMMUNITY STRATEGIC PLAN |

|

|||

|

FINANCIAL IMPLICATIONS |

There are no Financial implications associated with this report. |

|||

|

LEGISLATIVE IMPLICATIONS |

To comply with section 413 of the Local Government Act, 1993. |

|||

|

POLICY IMPLICATIONS |

Accounting Policies are detailed within the Financial Statements. |

|||

|

Nil |

|

1. The Mayor, Deputy Mayor, Acting General Manager and Responsible Accounting Officer be delegated to sign the Statements by Council and Management for the 2020 General Purpose Financial Statements and 2020 Special Purpose Financial Statements for Cootamundra-Gundagai Regional Council. 2. The 2020 Financial Statements be referred for audit. 3. The Acting General Manager be authorised to issue the 2020 Financial Statements upon receipt of the auditor’s report. |

Introduction

Section 413 of the Local Government Act, 1993 requires a resolution of Council to refer the draft financial statements to audit.

Section 413(2)(c) requires a resolution of Council that the annual financial statements have been prepared in accordance with;

· The Local Government Act, 1993 (as amended) and the Regulations made there under.

· The Australian Accounting Standard and professional pronouncements.

· The Local Government Code of Accounting Practice and Financial Reporting.

Further, that to the best of its knowledge and belief, the financial statements present fairly the operating result and financial position, and accord with Council’s accounting and other records.

Section 418 of the Act requires that as soon as practicable after Council receives a copy of the auditor’s report, it must fix a date for a meeting to present the audited financial statements to the public, and it must make the financial statements available for public inspection for at least seven days prior to the meeting date.

Discussion

The financial statements for the reporting period ended 30 June 2020 are currently being prepared and are scheduled for audit. Pursuant to section 413(1) of the Local Government Act, 1993 Council is required to refer the draft statements to audit.

A Councillor Workshop will be scheduled to allow for information and analysis to be provided.